Adapting to Inflation: The Necessity of Continuous Scenario Planning for a Sustainable Business

Publish Date: March 4, 2025Synopsys

The global economic landscape is witnessing a significant shift as inflation rates approach central bank targets, albeit slower, facilitating potential monetary easing across larger economies. The IMF’s (International Monetary Fund) Data report indicates that inflation, which peaked at 8.8% in late 2022, is projected to decline to 4.2% by the end of 2025 and to 3.5% in 2026, creating a more stable environment for financial institutions to navigate*1. Despite this positive trend, the global inflation rate remains susceptible to geopolitical tensions and commodity price fluctuations, necessitating proactive measures from financial entities.

Financial institutions are increasingly adopting scenario planning to manage the complexities of inflation and interest rate changes effectively. This strategic tool enables organizations to explore various “What if” scenarios, allowing them to stress-test their operations against potential inflation impacts. Regular scenario planning sessions help institutions identify risks and opportunities, ensuring they remain agile in a rapidly evolving economic climate.

Timely scenario planning is crucial for financial institutions to prepare for the complex challenges of inflation and shifting monetary policies. By anticipating different economic outcomes, these institutions can better align their strategies with both current realities and future uncertainties. This proactive approach enhances risk management and positions organizations to capitalize on emerging opportunities in a post-inflationary world.

In summary, as inflation stabilizes and central banks consider easing monetary policies, the importance of scenario planning cannot be overstated. It equips financial institutions with the insights needed to navigate potential disruptions in underlying factors while fostering resilience and stability in an unpredictable global economy.

The Situation

Since 2020, we have been experiencing an unstable inflationary trend worldwide. Meanwhile, central banks around the world have continued to adjust interest rates in response to inflation over the last few years.

Inflation manifests as an increase in the prices of goods and services, leading to a decline in the purchasing power of money. Inflation typically translates into elevated operational expenses for business owners and CEOs, pressuring operating margins. Conversely, financial institutions and lenders, responding to a contraction in the money supply orchestrated by central banks and the necessity to mitigate risk, tend to elevate interest rates on savings and credit products, which goes hand in hand with policy rates to tackle inflation. Also, an escalation in the federal budget deficit often correlates with increased government expenditure, frequently financed through debt issuance—to revitalize economic activity, which can further aggravate inflationary pressures. Such dynamics may strain financial firms’ revenue streams, capital adequacy ratios, or solvency reserves.

Recent observations indicate that economies exhibit “stickiness,” characterized by sluggish adjustments in prices and wages in response to shifting economic conditions, resulting in extended periods of inflation. This rooted behavior compels central banks to implement further interest rate hikes, which have had a relatively soft impact on banks and their clientele thus far.

The National Federation of Independent Business (NFIB, USA) survey reveals dual trends. The NFIB Small Business Optimism Index floated around 91% to 94% until October 2024, marking it below the 50-year average of 98.23%. Later, the US’s NFIB Small Business Optimism Index soared to 105.1% in December 2024 due to an improved economic outlook following the election*2. The small business owners reported that inflation was one of their most crucial business problems, with higher input and labor costs.

In another survey by Fed Small Business*3, “Most firms reported adverse effect due to increase in interest rates with an increased cost of debt being the most common effect.”

This blog tries to spotlight the latest voices heard from the BFSI sector’s end customers, which Financial Firms can consider when dealing with their clients.

The Problem Statement

How can banks or Financial Institutions effectively strategize when businesses are refining their models, unpredictable economic conditions, and technologies continually evolve?

Most financial firms are aware of these questions and their answers. However, determining how to answer them could be exploratory.

Impact on Banks

Let’s try to understand the direct impact of rate changes on Financial Institutions. Below are a few illustrative examples of how inflationary situations can affect Banks and Financial Institutions.

| Entities | Scenarios | It Can Affect | Goes down | Goes Up |

| Commercial Bank | Possibility of asset-liability mismatch resulting in less availability of credit for customers | Net Interest Income | Deposit growth rate | Expenses from interest-bearing liabilities |

| Asset Management | Falling Asset Under Management and increase in expenses | Fee and commission income | Total Transaction Value and charges | Operation expenses |

| Investment Bank | Delay in deals and higher deal cost | Trading Income | Volume of Trade Transaction | Underwriting risk |

| Bank Assurance | Rising prices increase the costs of credit insurance, mortgage insurance, and other premiums, potentially discouraging policy sales and causing lapses. | Brokerage and commissions,

Cross Selling Volume |

New Policy revenue and value of invested assets | Distribution cost |

Why does it happen

Inflation can adversely affect small businesses by diminishing consumer spending and sales. As the costs of raw materials and other operational expenses rise, production and operational costs also escalate. In the mortgage sector, real estate inflation often serves as an early indicator of potential credit issues. Effective collections and communication are crucial components of any credit offering. Common challenges faced by collections departments within financial institutions include limited human resources, a shortage of specialized personnel, the need for proactive notifications, timely communications, and time constraints. Financial institutions frequently encounter persistent challenges and obstacles during inflationary periods despite ongoing process improvements.

In an economy where the Banking Industry is making a transition, a new operating model may change how firms engage with their customers. Large/Small Banks, FIs, and Credit Unions will differentiate by improving their ability to interact with customers and prospects to maximize their value.

Financial firms can expect volatility in origination or collection as the economy and consumer sentiment remain dynamic in the coming period.

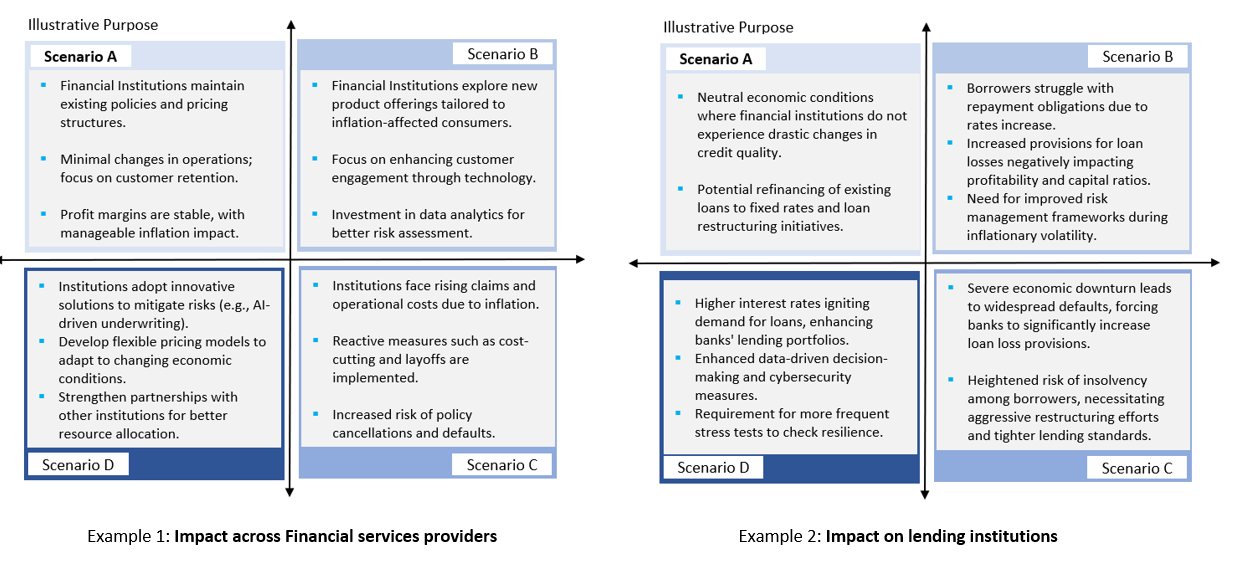

Discovery Framework

Here is an early scenario planning exercise to draft a solution. The grid generates four quadrants that help us to understand how the two variables interact. Each quadrant plots a different scenario. One quadrant may represent the “As-Is” or “Business as usual,” while the other suggests new directions for business to explore. The scenarios can be improvement, worsening, or any other situation.

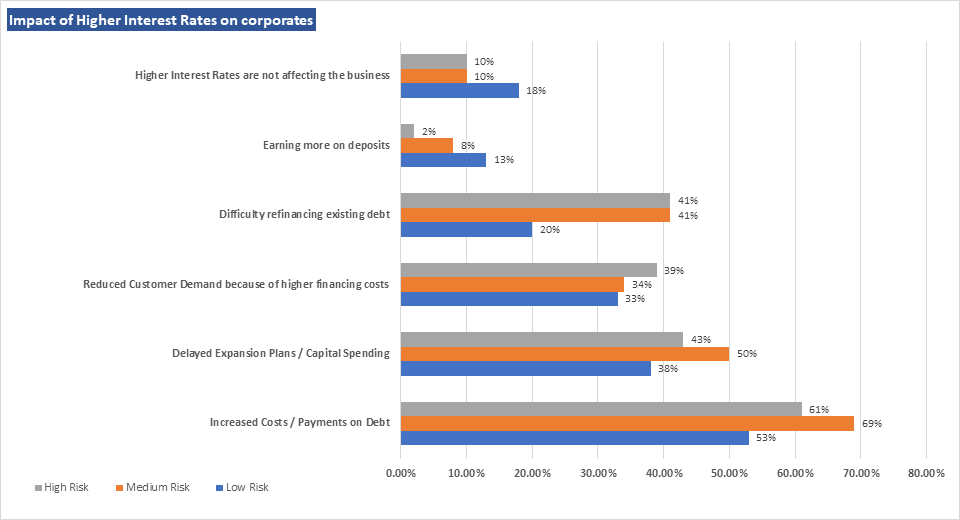

We have interpreted the impact on corporations (as shown in the survey above) in a volatile inflationary environment and how it impacts the financial services participants. The survey findings were made using scenarios and a couple of examples. The exercises cited here are for illustrative purposes only, and companies can develop customized scenarios for their problem statement.

How to Succeed

Although scenario planning and stress testing is a specialized activity, data-driven insights can augment a variety of factors to facilitate the planning process. Using digital technologies such as Artificial Intelligence, Machine Learning, and Generative AI provides a sustainable option for faster and more cost-effective coverage. Organizations must also upskill their employees and orchestrate change management processes to conduct various analysis activities utilizing the latest technology to maintain agility. Sensitivity analysis tools can be used to track the output against the variables. Below is one such example

| Sensitivity Analysis Tool (Illustrative) | ||

| Scenario | Inflation (example) | Impact |

| Impact of increase in | 1.00% | |

| Higher | Interest Rate | Expensive loans for customers |

| Reduced / Higher | Demand | A high interest rate environment makes loans unattractive / but reduced savings increase demand for loans. |

| Elevated | Default Rate | Caused by lower savings rate or increased expenses leading to stress on income levels or lower operating margins |

Conclusion

The interconnected organizations with their customers’ ecosystems and mutual interdependence are crucial factors for financial institutions operating in today’s economy. Below are several strategies to consider in this volatile environment:

- Developing Adaptive Capabilities: Continuously achieving the optimal balance within operational frameworks will be essential for survival.

- Real-Time Data Monitoring and Collaboration: Financial service providers assist their corporate clients in identifying patterns and managing complexities. Given the overwhelming volume of data and information, effective collaboration and systemic thinking through real-time monitoring are imperative.

- Scenario Testing: Implement stress testing scenarios, conduct what-if analyses, and utilize forward-looking predictive modeling through data analytics, process optimization, human resources, and strategic planning.

The analysis from this exercise can be linked to forward-looking financial impact through the rest of the budgeted timeline. Financial Institutions can help businesses mitigate most of their consumers’ problems or apprehensions through a proactive or adaptive solution and engage them in the whole process for a favorable situation.

Alternate investment offerings, payment relaxation, loss mitigation plans, or customer assistance programs can be proposed or customized to minimize the impact on both sides.

We at YASH BizNeXT Consulting facilitate customized approaches to BFSI clients to help them navigate challenges through our People, Process, and technology-centric consulting offerings. Value tracking and process mining are a few such consulting offerings. We help clients perform stress testing through as-is value from each business activity and compare it with the desired state, thereby recommending an action plan. Understanding the overall operation insight across the value chain is very important to support building operational resilience in adverse economic conditions. We use process insight and process mining data to observe the patterns and look for alternate solutions during a crisis. Talk to us at BizNeXT@yash.com about how we can help you solve such problems.